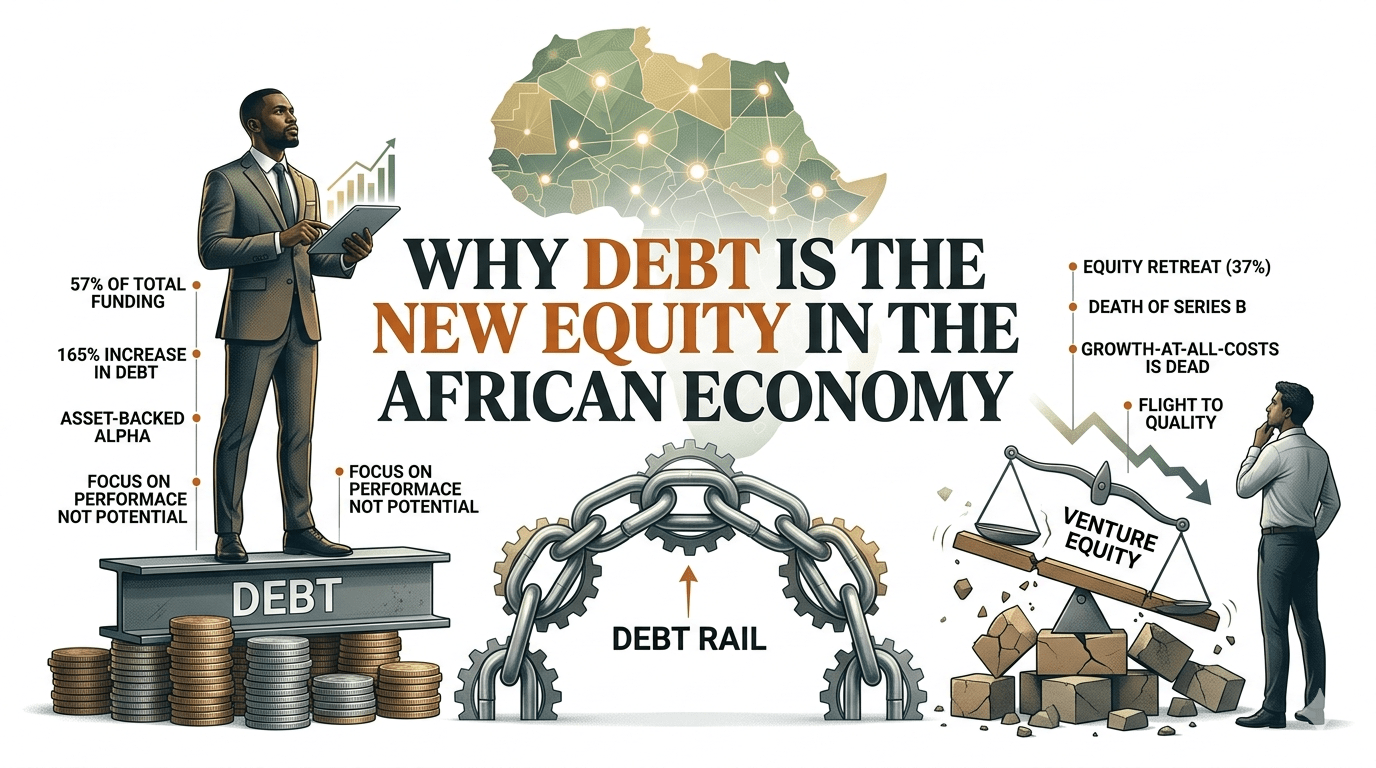

The narrative of “African Venture Capital” has hit a fundamental inflection point. For a decade, the dream was built on equity: selling pieces of the future to fund the losses of the present. Today, April 6, 2026, the Q1 data confirms a brutal but necessary reality: Investors no longer want to buy your “Potential”; they want to lend against your “Performance.” In the first three months of 2026, the composition of capital flipped. Debt financing rose by 165%, while Equity fell by 37%. This isn’t just a market dip—it is a Genetic Re-coding of how African companies are built.

1. THE INVESTIGATION: Tracking the $705 Million Total

While early mid-quarter trackers flagged $487 million, the final Q1 data settled at approximately $705 million across 59 deals. But the headline figure is a “Sovereign Illusion.”

When you strip away the layers, the core is hollowed out:

-

The Debt Dominance: Of that $705M, pure equity accounted for only $212 million. Debt and hybrid instruments claimed the remaining $493 million.

-

The “Concentration” Trap: Just five deals (SolarAfrica, ValU, Breadfast, GoCab, and Spiro) accounted for the vast majority of growth capital.

-

The Investor Exodus: The count of US-based investors dropped by 53% (from 30+ in early 2025 to 14 in 2026). In their place, Development Finance Institutions (DFIs) like the IFC and BII have moved from “Gap Fillers” to “Market Makers.”

2. CASE STUDY I: The Asset-Backed Alpha (SolarAfrica & ValU)

The rise of debt is not a sign of desperation; it is a sign of Operational Maturity. ### Scenario: South Africa’s SolarAfrica ($94M Project Debt)

SolarAfrica’s massive Q1 round from Rand Merchant Bank (RMB) and Investec is the 2026 blueprint. They aren’t selling equity to pay for software developers; they are using debt to build physical solar infrastructure.

-

The Logic: Debt is non-dilutive. For a company with predictable monthly subscription revenue from solar installations, borrowing at 12–15% is infinitely cheaper than selling 20% of the company to a VC.

-

The Result: They own the assets, the bank gets the interest, and the founders keep the equity.

Scenario: Egypt’s ValU ($63.6M Debt)

ValU, the lifestyle-enabled fintech, secured its debt from the National Bank of Egypt. This is “Balance Sheet Sovereignty.” By borrowing local currency to fund local loans, they eliminate the “FX Risk” that killed so many startups in 2024–2025.

3. THE “GROWTH SQUEEZE”: The Death of the Series B

The investigation reveals a terrifying gap in the “Scaling Ladder.” In Q1 2026, Series B rounds effectively dropped to zero.

-

The “Flight to Quality”: Investors are terrified of the “Middle Zone.” They are happy to write $1.6M seed cheques (the current Nigerian average) or participate in $50M debt facilities for titans. But the $15M–$25M Series B—the round where you prove you can scale—has become a “Death Valley.”

-

The Multiplier Effect: Because global interest rates remain high, the “Cost of Capital” for a VC is now higher than the expected return of a mid-stage African startup. VCs are now demanding 20% EBITDA margins before they even look at a Series B pitch.

4. CASE STUDY II: The Mobility “Centaur” (Spiro & MAX)

Mobility tech (EVs and logistics) pulled in $161 million this quarter. This sector is the primary driver of the debt trend because it is Asset-Heavy.

Tracing the “Max” and “Spiro” Playbooks:

-

Spiro (Benin/Togo): They are building battery-swapping stations. This is hard infrastructure. You cannot fund 10,000 electric bikes and 500 charging stations with “Venture Equity”—the dilution would be 90%.

-

The Strategy: They use equity to build the technology and Debt to buy the bikes. * Case Study: GoCab (Côte d’Ivoire) raised $45 million in Q1. They are not a “Software App”; they are a Logistics Utility.

5. THE “MISSING MIDDLE”: The Private Debt Opportunity

As equity retreats, a new asset class has emerged: Private Debt Funds.

-

GIF Growth Case Study: Funds like GIF Growth are now targeting the $1M–$5M debt range. Why? Because 73% of African startups need loans longer than two years to smooth out receivables and inventory.

-

The Revenue-Share Pivot: We are seeing the rise of Revenue-Based Financing (RBF). Startups are repaying their capital as a percentage of monthly revenue rather than a fixed interest rate. This aligns the investor with the company’s actual cash flow.

6. REGIONAL TRACER: Who is Winning the Shift?

| Country | Total Q1 Capital | Debt % | Strategic Lead |

| Egypt | $190 Million | 65% | Debt-funded FinTech & E-commerce (Breadfast). |

| South Africa | $157 Million | 80% | Climate Tech & Infrastructure. |

| Kenya | $114 Million | 40% | E-mobility & Agri-Tech. |

| Nigeria | $78 Million | 15% | High volume of Seed deals, but lacking Growth Debt. |

7. THE INVESTIGATION CONCLUSION: The 2026 Mandate

The shift from Equity to Debt is the Professionalization of African Tech. Startups are finally being treated like Businesses rather than Experiments. If you can show cash flow, the banks are now open. If you are still “Pre-Revenue” and chasing a Series B, you are in a survival race against a clock that no longer resets with a new pitch deck.

In the 2026 economy, Equity is for Vision; Debt is for Scale. The “Titan” of the next decade won’t be the founder who raised the most VC money; it will be the one who built the most resilient balance sheet.

Sources & References (Verified April 6, 2026)

-

Condia Funding Tracker (Apr 2026): African startups raise $705M in Q1 2026 as debt surges

-

Techmoonshot Analysis (Apr 2, 2026): Africa’s Most Active Startup Investors in Q1 2026

-

Partech Africa Annual Report (Jan 2026): 2025 Africa Tech Venture Capital – The Rise of Debt

-

Global Innovation Fund (Feb 2025): Unlocking private debt for African startup growth