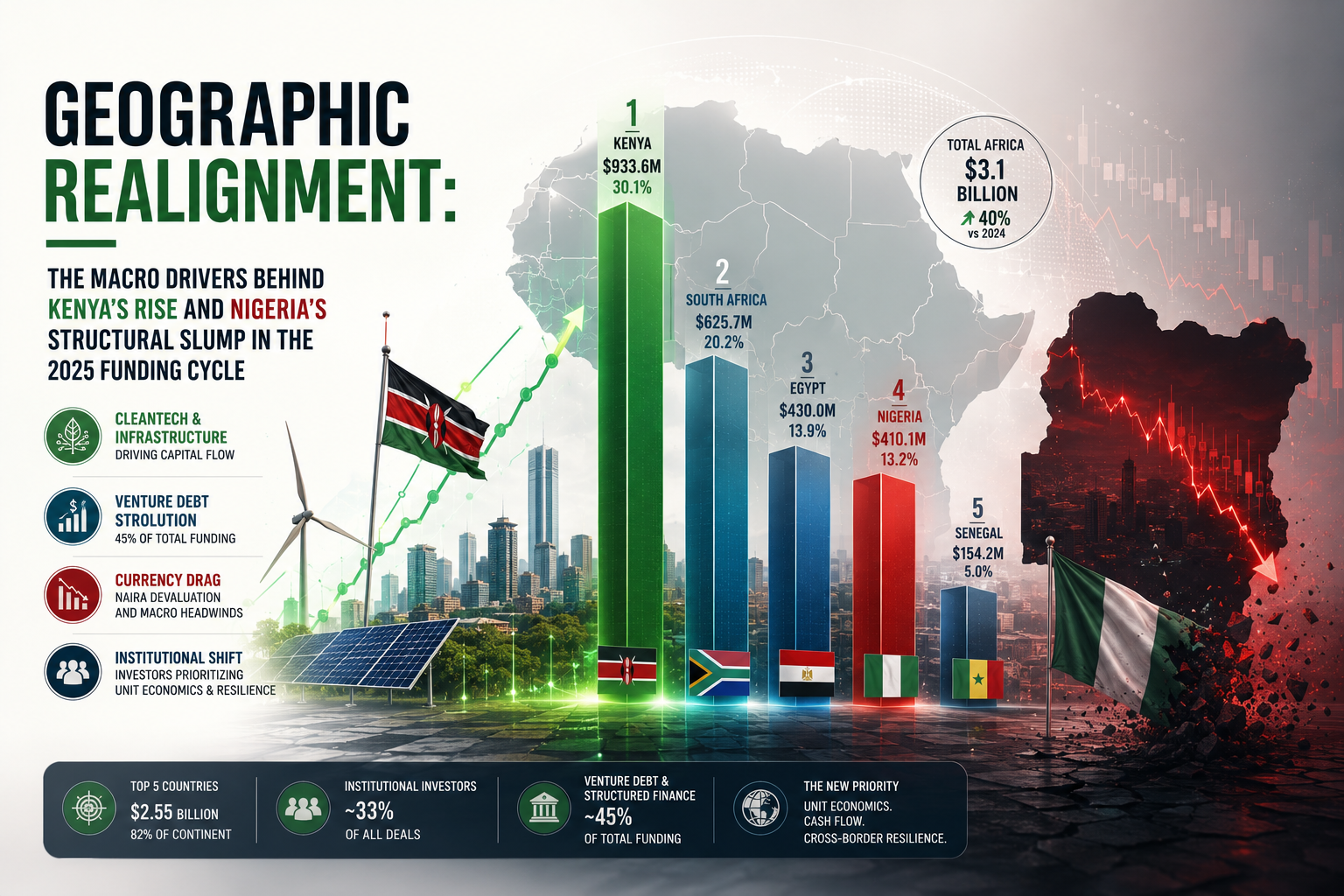

The African venture ecosystem experienced a sharp, structural reset in 2025. Total startup funding across the continent rebounded to $3.1 billion—a significant 40% increase from the $2.2 billion recorded during the macroeconomic correction of 2024.

However, beneath this headline recovery lies a fundamental geographic and asset-class realignment. For the first time in modern African tech history, Nigeria has been unseated as the undisputed capital destination on the continent.

According to consolidated ecosystem data from Launch Base Africa and Statisense, funding concentration remains aggressively top-heavy, with the top five countries capturing $2.55 billion—accounting for 82% of all venture allocation in Africa. Yet, the internal balance of power within this “Big Four” framework has completely inverted.

The 2025 Sovereign Funding Landscape

| Rank | Country | Total Capital Raised (2025) | Market Capture (% of Continent) |

| 1 | 🇰🇪 Kenya | $933.6M | ~30.1% |

| 2 | 🇿🇦 South Africa | $625.7M | ~20.2% |

| 3 | 🇪🇬 Egypt | $430.0M | ~13.9% |

| 4 | 🇳🇬 Nigeria | $410.1M | ~13.2% |

| 5 | 🇸🇳 Senegal | $154.2M | ~5.0% |

Deconstructing the Shift: Why Kenya Pulled Ahead

Kenya’s rise to the top spot, capturing nearly one-third of the continent’s total venture capital, reflects a deliberate shift in global investor appetite away from pure-play consumer software toward hard asset infrastructure and climate-tech resilience.

-

The Cleantech and E-Mobility Surge: Kenya has become the primary testing ground for large-scale climate infrastructure. Massive capital injections into off-grid solar providers like Sun King (which secured a landmark $156 million securitization facility) and electric mobility pioneers like Spiro ($100 million) anchored the nation’s dominant position.

-

The Venture Debt Revolution: Across the continent, venture debt and structured project finance scaled rapidly to comprise nearly 45% of total funding raised. Because cleantech, logistics, and electric mobility rely heavily on physical assets and predictable asset-backed revenue streams, Kenyan operators successfully unlocked deep debt tranches from global commercial banks and Development Finance Institutions (DFIs).

The Currency Drag: What Slipped in Nigeria?

Nigeria’s descent to fourth place ($410.1 million) is not an indictment of its entrepreneurial capacity, but rather a direct reflection of severe macroeconomic headwinds.

“The continued structural devaluation of the Nigerian Naira fundamentally altered the underwriting model for international venture capitalists. Consumer-facing startups generating revenues in local currency struggled to outrun FX devaluations when reporting dollar-denominated returns to global LPs.”

The ongoing currency correction, paired with high domestic inflation, severely compressed household disposable income. This directly exposed the vulnerability of high-frequency, low-margin B2C fintech applications and e-commerce platforms that dominated Nigeria’s historic funding boom. While infrastructure-centric fintech giants like Moniepoint still closed massive growth equity extensions (including a $200 million Series C), the broader retail software layer saw compressed valuations and an institutional capital freeze.

Strategic Outliers: South Africa, Egypt, and the Francophone Wedge

-

South Africa ($625.7M): Benefiting from its highly sophisticated domestic capital markets, deep local institutional funds, and stable corporate governance structures, South Africa maintained a resilient second place. The ecosystem also proved its maturity through major exit events, highlighted by Optasia’s $1.4 billion listing on the Johannesburg Stock Exchange (JSE).

-

Egypt ($430.0M): Egypt defended its third-place position by acting as a strategic bridge between North Africa and the Middle East, commanding heavy volumes in proptech (such as Nawy’s $75 million raise) and digital B2B commerce.

-

Senegal ($154.2M): Holding the fifth spot, Senegal’s strong performance proves that Francophone West Africa is graduating from a Tier-2 alternative into a highly institutional ecosystem, anchored heavily by regional financial infrastructure rails like Wave.

The 2026 Outlook

The data demonstrates that the era of funding generalized “software ideas” on the continent has drawn to a close. International and local institutional investors—who now account for nearly one-third of all active transactions—are prioritizing unit economics, clear paths to cash-flow viability, and cross-border hedge capability. For founders entering the next funding cycle, matching capital requests with asset-backed instruments or clear FX-insulated revenue models will remain the definitive prerequisite for securing runway.