For decades, the African defense narrative was a story written in foreign languages. From the Cold War-era surplus of the East to the high-priced hardware of the West, Africa was the world’s most consistent consumer and its least significant producer. But as we move through 2026, the continent is undergoing a “Great Decoupling.” The goal is no longer just “security”; it is Strategic Autonomy.

We are transitioning from an era of dependence to a “Defense Prime” model, where indigenous startups—led by Terra Industries—are treating national security not as a government contract, but as a high-growth technology stack.

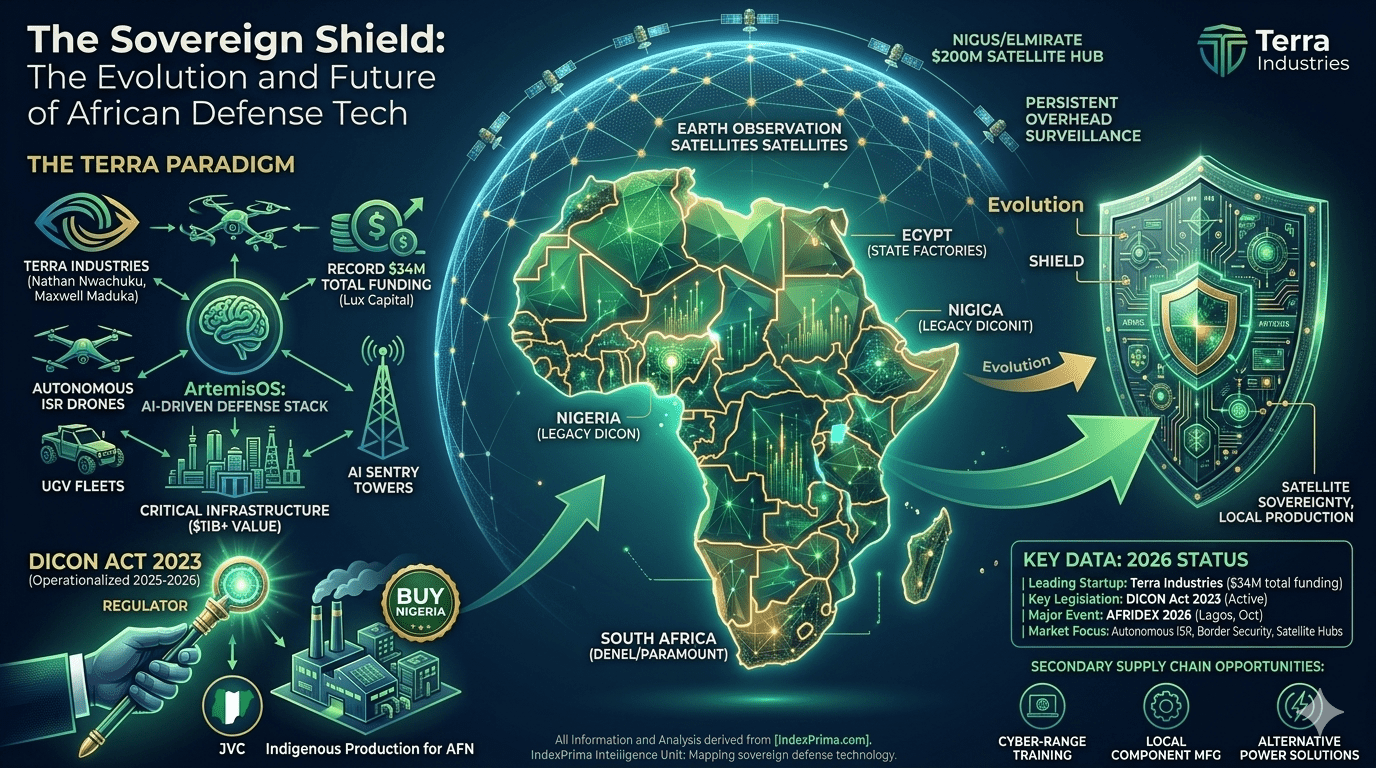

The Sovereign Shield: The Evolution and Future of African Defense Tech

The Historical Rearview: From “Import Only” to Industrialization

Traditionally, African defense was characterized by three regional hubs with very different origins:

-

South Africa: Built the continent’s only full-scale military-industrial complex during the apartheid era due to global sanctions. Companies like Denel and Paramount Group set the early standard for African armored vehicles and aerospace.

-

Egypt: Focused on massive state-owned factories, often assembly lines for Western or Eastern designs under license.

-

Nigeria: Historically relied on the Defence Industries Corporation of Nigeria (DICON), which for decades remained a bullet-and-rifle manufacturer, largely stagnant while the world moved toward digital warfare.

The Present: A Continental Shift (Region by Region)

1. West Africa: The “Terra” Paradigm and the Rise of AI

The most significant move in 2026 is the meteoric rise of Terra Industries (formerly Terrahaptix). Founded by young Nigerians Nathan Nwachuku and Maxwell Maduka, the company has become the “Anduril of Africa.”

-

The Capital Signal: In February 2026, Terra raised a $22 million Seed Extension led by Lux Capital, bringing their total funding to $34 million. This isn’t just a win for Terra; it is a signal that Silicon Valley now views African defense tech as a VC-backable asset class.

-

ArtemisOS: Their proprietary moat. ArtemisOS is an AI-powered operating system that coordinates autonomous drones, unmanned ground vehicles (UGVs), and sentry towers. It currently protects over $11 billion in critical infrastructure, from oil rigs in the Delta to mining sites in the North.

-

The Regulatory Catalyst: The DICON Act 2023 has finally been operationalized. It transformed DICON from a competing manufacturer into a Regulator + Partner. The February 2026 Joint Venture (JVC) between DICON and Terra means Nigeria’s next generation of drones will be “Born in Nigeria, for Nigeria,” ending the reliance on Turkish or Chinese exports.

2. North Africa: The Drone Hub

Egypt and Morocco have shifted focus toward unmanned aerial systems (UAS). Morocco, in particular, has leveraged its partnership with Israel (BlueBird Aero Systems) to begin local production of suicide drones and ISR (Intelligence, Surveillance, Reconnaissance) platforms.

-

The Logic: In 2026, North African states are using these indigenous drones to secure vast desert borders where traditional patrols are economically impossible.

3. Southern Africa: The Hardware Pivot

While Paramount Group continues to export the Marauder armored vehicle globally, the new focus is on Cyber-Defense. South Africa is becoming the regional hub for military-grade encryption and secure communication hardware, protecting the SADC region’s digital sovereign borders.

The Future: The $200M Satellite and Tactical Hub

In March 2026, a landmark $200 million deal between Nigus International and Elmirate Capital was signed to launch a next-generation defense tech and satellite hub in Nigeria.

-

The Problem: Currently, African nations spend billions renting satellite imagery from foreign providers to track insurgents.

-

The Solution: Local production of Earth Observation Satellites. This move provides Nigeria with “Persistent Overhead Surveillance,” making border incursions visible in real-time without needing permission from a foreign power to access the feed.

The “IndexPrima” Verdict: Defense is the New Fintech

The Nigerian elite have realized that security is the bedrock of all other economic activity. Defense tech is currently where Fintech was in 2016—on the verge of an explosion. For B2B founders and investors, the “Gold Mine” is in the Secondary Supply Chain:

-

Cyber-Range Training: Providing virtual environments for the military to train on ArtemisOS and other AI platforms.

-

Precision Component Manufacturing: Localizing the production of carbon fiber, specialized sensors, and high-performance batteries.

-

Alternative Power Solutions: Building hydrogen or solar-powered “Silent Bases” that can operate in remote areas without the logistics trail of diesel fuel.

| Metric | 2026 Status |

| Leading Startup | Terra Industries ($34M total funding) |

| Key Legislation | DICON Act 2023 (Domesticated & Active) |

| Major Event | AFRIDEX 2026 (Lagos, Oct 2026) |

| Market Focus | Autonomous ISR, Border Security, Satellite Hubs |

Sources & Strategic References:

-

Investment Intelligence: Lux Capital leads record-breaking seed for Terra Industries (Financial Times/TechCrunch, Feb 2026).

-

Legislative Record: DICON Act 2023: The Modernization of the Nigerian Defence Industrial Complex (Federal Gazette, 2023/2025).

-

Regional Case Study: Morocco-Israel Defense Production Agreement: A New Era for North Africa (Defense News, 2025).

-

Space Intelligence: Nigus & Elmirate $200M Satellite Hub: Analysis of Nigerian Space Sovereignty (IndexPrima Intelligence Unit, March 2026).