For the past two years, the African tech ecosystem has been defined by a “wait-and-see” approach—a period of survival where “burn” was a dirty word and profitability was the only north star. But as we close the first quarter of March 2026, the data suggests we have moved past mere survival into a sophisticated rebound and recalibration.

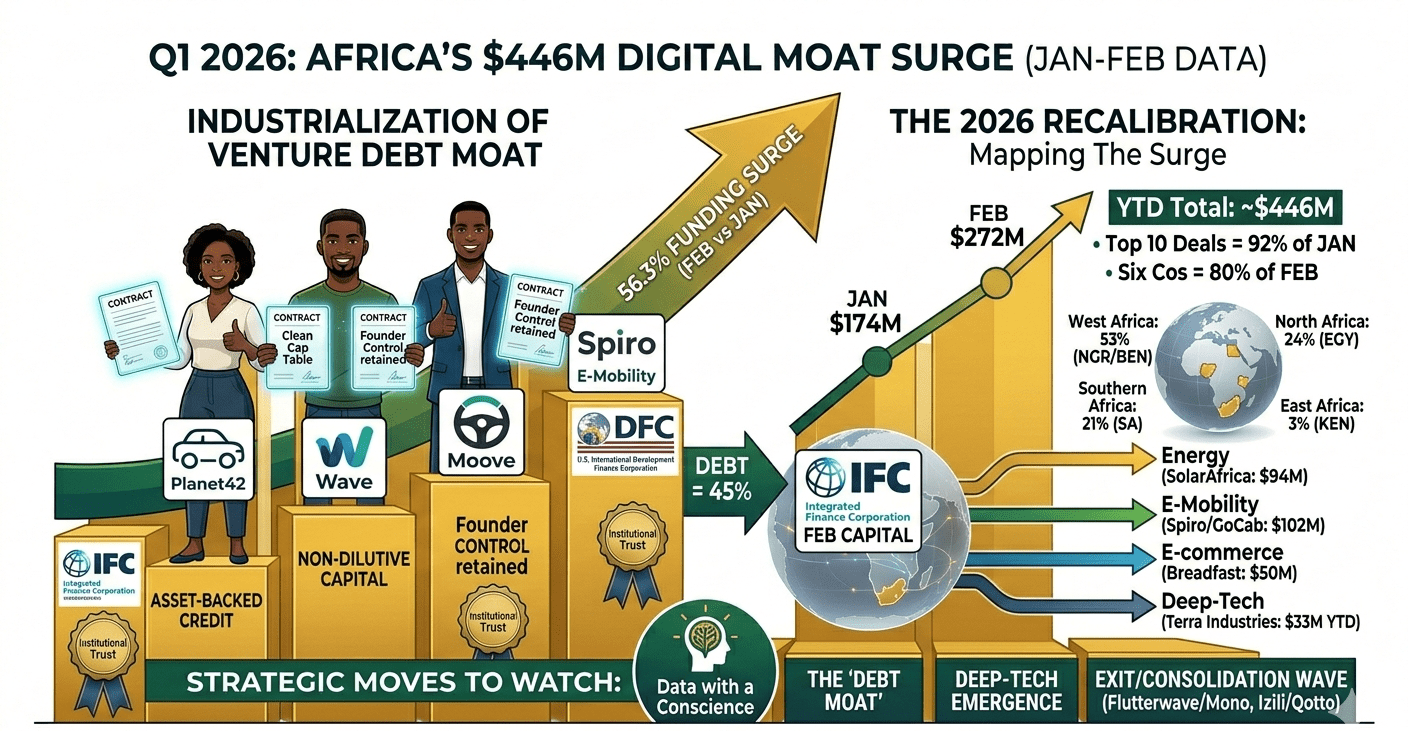

The numbers tell a story of concentrated strength. While January opened with a cautious, selective gait, February detonated with a 56.3% surge in capital inflow. In just sixty days, the continent’s top-tier startups pulled in approximately $446 million, signaling not just a recovery of appetite, but a fundamental shift in how that appetite is satisfied.

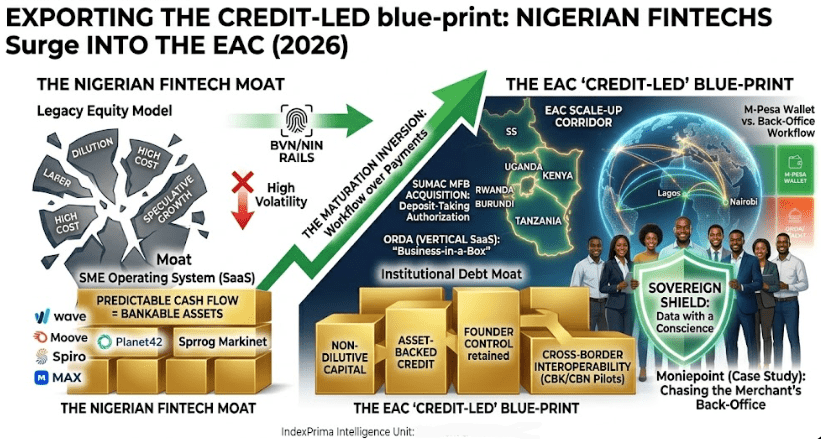

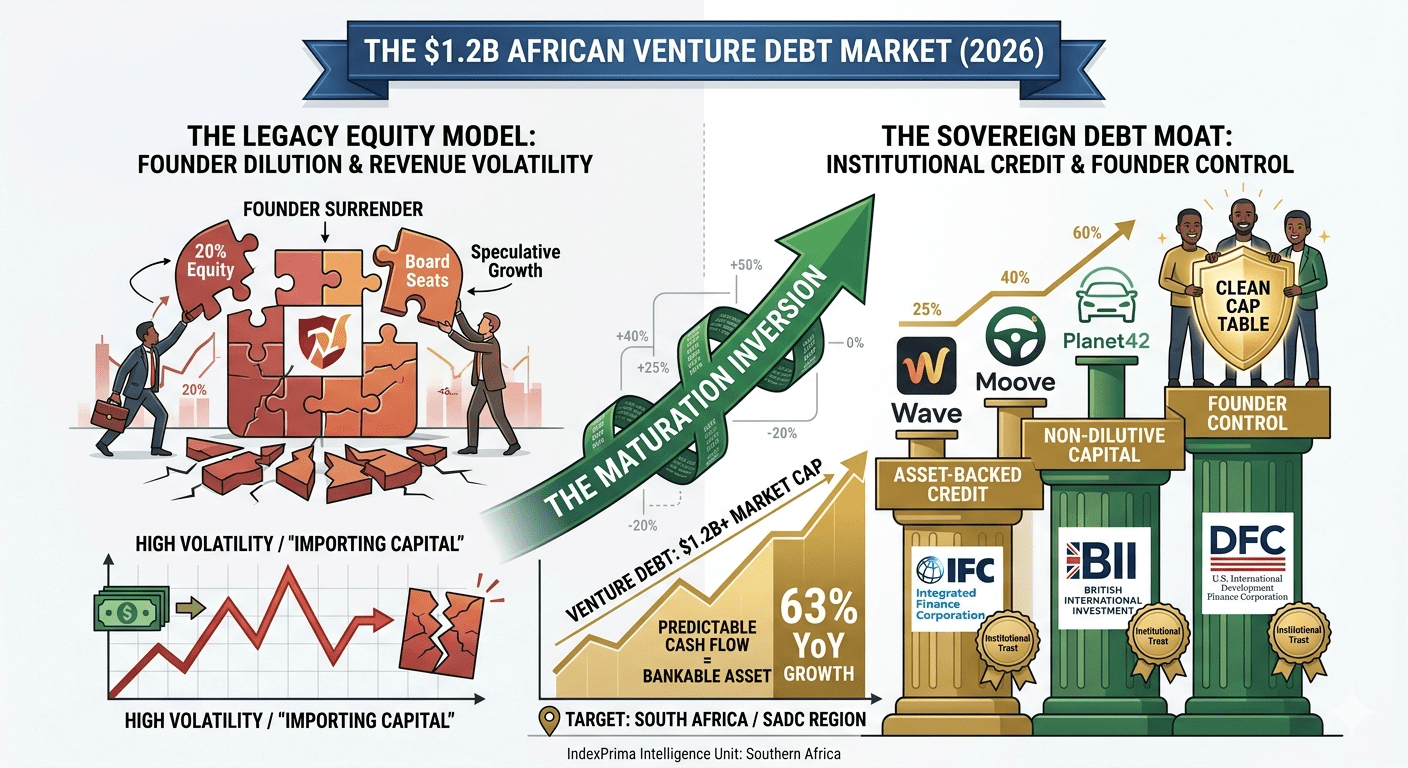

This is no longer a market obsessed with “growth at all costs.” In 2026, the Venture Debt Moat has arrived, fundamentally altering the cap tables of the continent’s most promising scale-ups.

1. The January “Selective” Start: Concentration is the New Alpha

January 2026 ($174M – $177M) was a masterclass in high-conviction investing. It was characterized by extreme capital concentration, with the top 10 deals capturing a staggering 92% of all investment. Investors weren’t spreading bets; they were doubling down on infrastructure-heavy winners.

| Company | Sector | Country | Amount | Type |

| valU | Fintech | Egypt | $64M | Debt (from NBE) |

| MAX | Mobility/Fintech | Nigeria | $24M | Equity & Debt |

| NowPay | Fintech | Egypt | $20M | Not Specified |

| Yakeey | Proptech | Morocco | $15M | Series A |

| Terra Industries | Defense/Deeptech | Nigeria | $11.75M | Infrastructure Expansion |

| Cauridor | Fintech | Côte d’Ivoire | $9.5M | Seed |

The Strategic Pivot: The $64M debt facility for valU in Egypt set the tone for the year. It proved that legacy financial institutions, like the National Bank of Egypt (NBE), are now comfortable acting as the primary liquidity providers for high-growth fintech platforms. Meanwhile, Flutterwave’s acquisition of Mono ($30M valuation) signaled that the “Super-App” war in West Africa is moving into its consolidation phase.

2. The February Infrastructure Explosion: Hardware Wins

If January was about finance, February ($272M) was about Hardware and Energy. Six companies alone captured 80% of the month’s total funding, marking a massive pivot toward logistics and green infrastructure.

| Company | Sector | Country | Amount | The “Index” Insight |

| SolarAfrica | Energy | South Africa | $94M | The largest deal YTD; tackling the energy moat. |

| Spiro | E-Mobility | Benin | $57M | Strategic debt to power EV expansion. |

| Breadfast | E-commerce | Egypt | $50M | Pre-Series C; dominating the Cairo grocery stack. |

| GoCab | Ride-hailing | Côte d’Ivoire | $45M | Blended capital for Francophone scale. |

| Terra Industries | Deep-tech | Nigeria | $22M | Validating the African Defense-Tech market. |

The Deep-Tech Emergence: The most provocative story of Q1 is Terra Industries. By raising over $33M YTD for defense and hardware manufacturing in Nigeria, they have broken the “Software-Only” curse. Investors are finally acknowledging that Africa’s biggest problems—security and infrastructure—require physical, industrial-grade solutions.

3. Regional Dominance: The New Leaderboard

The “Big Four” remain the pillars, but the internal hierarchy is shifting.

West Africa (53%): Nigeria remains the heavyweight champion, but the emergence of Benin (via Spiro) and Côte d’Ivoire (via GoCab) shows that the “Francophone Surge” is no longer a myth—it is an industrial reality.

North Africa (24%): Egypt continues to lead in fintech and grocery tech, leveraging its proximity to both Gulf capital and Mediterranean trade routes.

Southern Africa (21%): Led by South Africa’s mature energy and venture debt markets. It remains the most “bankable” region for institutional credit.

East Africa (3%): A surprising “cooldown” phase. After years of dominance, Kenya is currently seeing a lull in mega-deals as the market waits for the next cycle of e-mobility exits.

4. Three Structural Moves to Watch

A. The Rise of the Debt Moat

Debt now accounts for nearly 45% of all capital raised in February. For founders, this is the ultimate “Inversion.” Instead of selling equity at a discount, scale-ups with physical assets (EV bikes, solar grids, medical hardware) are using debt to grow. This allows them to scale without heavy dilution, keeping the “Sovereign Control” in the hands of the founders.

B. The Defense and Deep-Tech Alpha

The $33M+ raised by Terra Industries signals a “Defense-Tech” boom. As regional security becomes a priority for sovereign states, the B2G (Business-to-Government) sector is becoming the most lucrative frontier for African hardware founders.

C. The Exit and Consolidation Wave

Flutterwave/Mono and Izili Group/Qotto are just the beginning. 2026 will be the year of “Strategic Mop-ups.” Stronger players with cash-rich balance sheets are acquiring the “Infrastructure” of their competitors to build regional monopolies.

Sources & Strategic Intelligence

Market Tracking: Africa Tech Venture Capital Q1 2026 Real-Time Tracker (Africa: The Big Deal, 2026).

Deal Brief: SolarAfrica Secures $94M to Revolutionize South African Energy Grids (SolarAfrica Corporate, Feb 2026).

Regional Intelligence: The Rise of Francophone Tech: Côte d’Ivoire and Benin’s Record Q1 (TechCabal, March 2026).

The first quarter of 2026 has proven that the “African Tech Winter” didn’t kill the ecosystem—it forced it to grow up. We are now seeing a market that values hardware over hype and credit over cash-burn.