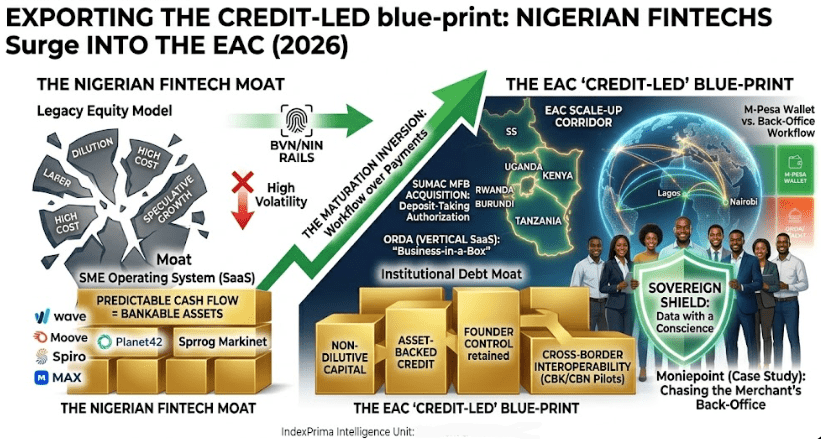

For years, the story of African fintech was told through the lens of payments. Success was measured by transaction speed, wallet adoption, and the “unbundling” of traditional banks. But as we move through March 2026, a new chapter has opened: the era of the SME Operating System. Nigerian fintech giants—having battle-tested their models in Africa’s most fragmented and high-volume retail market—are now exporting a sophisticated “Credit-Led Growth” blueprint to the East African Community (EAC). Leading this charge is Moniepoint, whose strategic acquisition of Sumac Microfinance Bank in Kenya (finalized March 27, 2026) serves as the definitive case study for this continental shift.

1. From Payments to “Business-in-a-Box”

The legacy model for entering a new market involved securing a Payment Service Provider (PSP) license and fighting for a slice of the transaction fee pie. Nigerian firms like Moniepoint, OPay, and PalmPay have realized that payments are a commodity; workflow is the moat.

By acquiring Orda Africa (a restaurant management vertical) alongside Sumac MFB, Moniepoint is moving beyond being a “wallet” to becoming the Operating System for Kenyan merchants.

Vertical SaaS: Instead of a generic POS, they provide software tailored to specific industries (e.g., restaurants, retail).

Embedded Finance: By running the merchant’s payroll, inventory, and digital menus, the fintech sees the business’s health in real-time.

The Inversion: They don’t ask for collateral; they use proprietary data from the software to offer instant working capital.

2. The Regulatory “Inversion”: Buying the Trust

Expanding into the EAC, particularly Kenya, has historically been a graveyard for foreign fintechs due to the Central Bank of Kenya’s (CBK) conservative licensing regime. Nigerian firms are now utilizing an “Acquisition First” strategy to bypass these barriers.

| Feature | Legacy Expansion (2020-2024) | The “Sovereign” Expansion (2026) |

| Market Entry | Apply for new PSP/Digital Lending licenses. | Acquire Majority Stakes in Tier-3 Banks. |

| Licensing | Years of “Regulatory Sandbox” waiting. | Immediate Deposit-Taking Authorization. |

| Strategy | Disrupt the incumbents. | Absorb the incumbents’ infrastructure. |

| Risk Model | Algorithmic (often predatory) lending. | Cash-flow based business banking. |

By taking a 78% stake in Sumac MFB, Moniepoint inherited 20 years of regulatory history and a deposit-taking license, turning a potential three-year wait into an overnight market entry.

3. Exporting the “Credit-Led” Blueprint

Nigeria’s fintech success was built on a harsh reality: in a high-inflation environment, cash is expensive. SMEs don’t just need a way to receive money; they need a way to access it.

Nigerian firms are exporting three core pillars of this credit-led model to the EAC:

Tiered KYC & Identity Rails: Leveraging Nigeria’s experience with BVN/NIN to help Kenyan regulators harmonize digital ID for credit scoring.

Inventory-Linked Credit: Providing loans that are automatically settled via a percentage of daily digital sales, reducing default risk.

Cross-Border Interoperability: As seen in recent CBN Policy Insights, Nigeria is pushing for bilateral pilots with Kenya and Ghana for mutual recognition of fintech licenses, potentially creating a “passport” for African startups.

4. The Competitive Fallout: M-Pesa vs. The New Guard

In Kenya, the primary incumbent is Safaricom’s M-Pesa. While M-Pesa dominates the consumer “wallet,” the Nigerian “Operating System” model targets the merchant’s back-office.

The M-Pesa Gap: M-Pesa tells you that you were paid.

The Moniepoint Value: The Operating System tells you what was sold, who sold it, and how much credit you’ve earned for tomorrow’s restock.

We are witnessing the Industrialization of African Fintech. The export of Nigerian credit-led models to the EAC proves that the next decade of growth won’t come from “unbundling” the bank, but from becoming the merchant’s most essential employee.