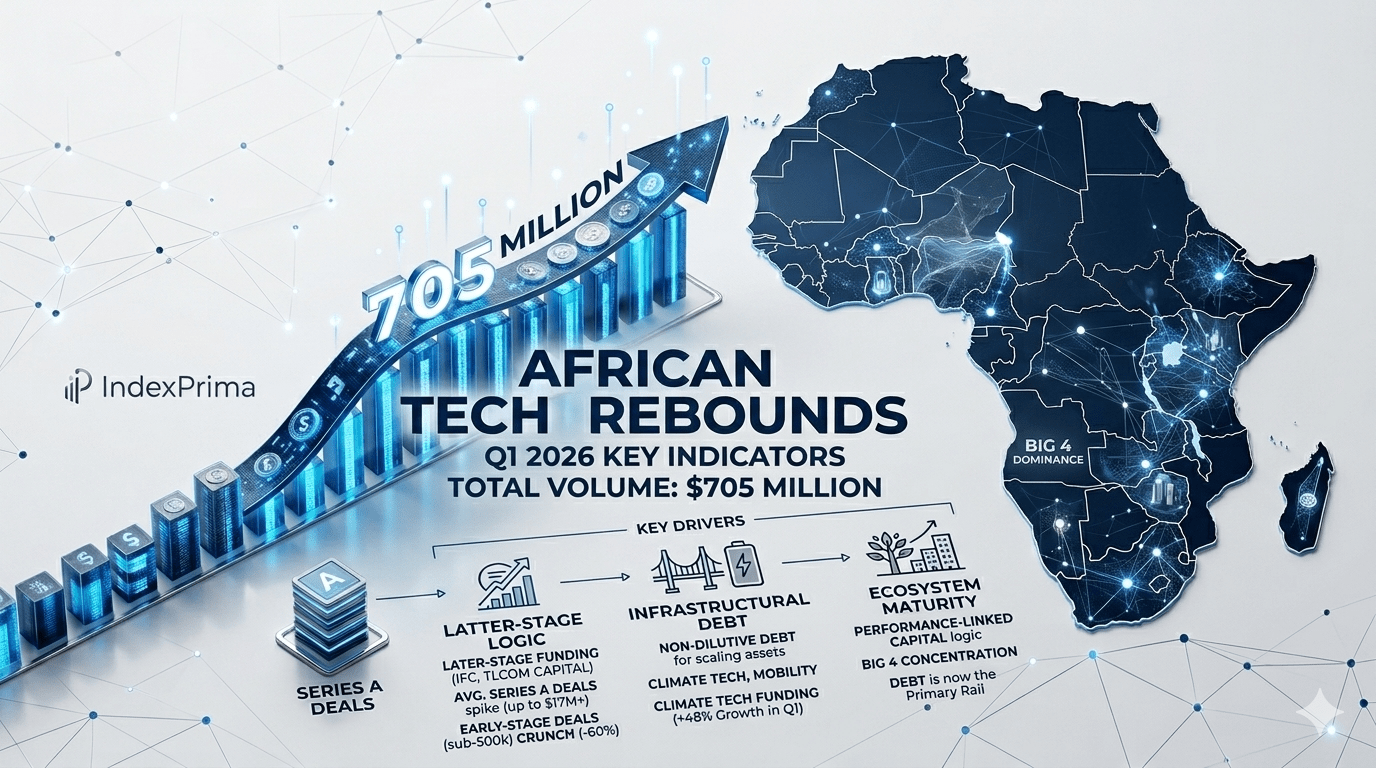

The African venture capital ecosystem has entered a period of Structural Reconfiguration. While the headline figure of $705 million raised in Q1 2026 suggests a robust 26.5% rebound from the previous year, the underlying mechanics reveal a market that has traded “experimentation” for “infrastructure.”

As of May 2026, the era of pure equity-driven growth is being replaced by a Hybrid Capital Model, where debt is now the primary engine of liquidity.

I. THE LIQUIDITY SHIFT: Debt Overtakes Equity

The most significant trend in early 2026 is the emergence of Venture Debt as a market maker rather than a backup plan.

-

The Debt Boom: Of the $705 million raised in Q1, debt and hybrid instruments accounted for over $490 million, while pure equity trailed at roughly $212 million. For the first time in the history of African tech, debt has surpassed equity in total capital volume for a single quarter.

-

Strategic Maturity: This shift is driven by mature companies—such as ValU ($63.6M debt) and SolarAfrica ($94M debt)—opting for non-dilutive capital to finance assets like solar installations and credit books.

II. TOP ACTIVE INVESTORS (Q1 2026 Scorecard)

Institutional investors have stepped into the vacuum left by the retreat of U.S. growth funds (whose participation dropped by 53% year-on-year).

| Investor | Profile & Strategy (2026 Status) |

| IFC | The Market Leader. The single most active investor in Q1 2026 by deal count, participating in 4+ deals across diverse sectors. |

| Partech Africa | Focused on Series A/B fintech. Currently deploying from its €280M+ fund with a strong presence in Dakar and Lagos. |

| TLcom Capital | Aggressively backing Seed to Series A infrastructure, particularly in North Africa and the “Big Four.” |

| Ventures Platform | The primary rail for early-stage Nigerian tech, deploying a $64M+ fund into fintech and health-SaaS. |

| Launch Africa | The “High-Frequency” investor, maintaining the highest volume of early-stage transactions across the continent. |

| Novastar Ventures | Pivoting toward Climate Tech and Mobility; recently closed its $147M “People and Planet” Fund III. |

III. THE GROWTH PARADOX: Concentration & The “Missing Middle”

The 2026 landscape is defined by Concentration—both geographically and in deal stages.

-

The Big Four Dominance: Egypt led the pack in Q1 with $190 million (driven by ValU and Breadfast), followed by South Africa ($157M), Kenya ($114.5M), and Nigeria ($78M).

-

The Early-Stage Crunch: Startups seeking $100k–$500k are facing a “SaaS-pocalypse.” Pre-seed and seed deal volumes have declined as investors pivot toward companies with “Physical Moats”—electric vehicles, batteries, and cold-chain logistics.

-

Series A Surge: For those who make it, the rewards are larger. The average Series A deal size has spiked, often reaching $17 million or more, as investors consolidate their capital into “survivor” companies with proven unit economics.

IV. SECTOR EVOLUTION: Beyond Fintech

While fintech remains the volume leader (accounting for ~$221M), the “Alpha” has shifted to infrastructure-heavy sectors.

-

Climate Tech (+48% Growth): Driven by the need for sovereign energy, climate tech saw a massive surge, highlighted by SolarAfrica’s $94M round.

-

Mobility & EV Infrastructure: Startups like GoCab ($45M in Côte d’Ivoire), Zeno ($25M), and MAX ($24M) are building the physical rails of African transport.

-

B2B Logistics: Logistics companies secured $149 million in Q1, signaling that the digital economy is now being anchored by physical delivery systems.

V. THE FOUNDER PLAYBOOK: Navigating 2026

For founders raising in the current environment, the “Rules of the Rail” have changed:

-

Hard-Code Sustainability: Investors are no longer funding “users.” They are funding Cash Flow. If your CAC (Customer Acquisition Cost) is higher than your LTV (Lifetime Value), you are uninvestable in 2026.

-

Build Physical Moats: Software alone is no longer a defense. Integration with hardware, logistics, or energy infrastructure is the new gold standard for attracting institutional debt.

-

Target Africa-Focused VCs: Traditional U.S. growth funds have largely withdrawn. Your primary path to capital now lies with TLcom, Partech, Enza, and Development Finance Institutions (DFIs) like the IFC.

The “Index” Take: In 2021, the African tech story was about “Potential.” In 2026, it is about “Performance.” The rebound to $705 million is a sign of a maturing market that has learned to build through a “Venture Winter.” The companies that survive this cycle will be the ones that own the physical and financial rails of the continent.

References & Sources:

-

[1] Empower Africa: African Startups Raise $705 Million in Q1 2026

-

[2] TechMoonshot: Africa’s Most Active Startup Investors in Q1 2026

-

[3] Africa: The Big Deal: Debt Overtakes Equity in African Tech Funding (Q1 2026 Report)

-

[4] Tech In Africa: African Startup Funding Trends: The Rise of Venture Debt

-

[5] Launch Base Africa: Series A Contracts while Debt Expands (Q1 2026 Analytics)