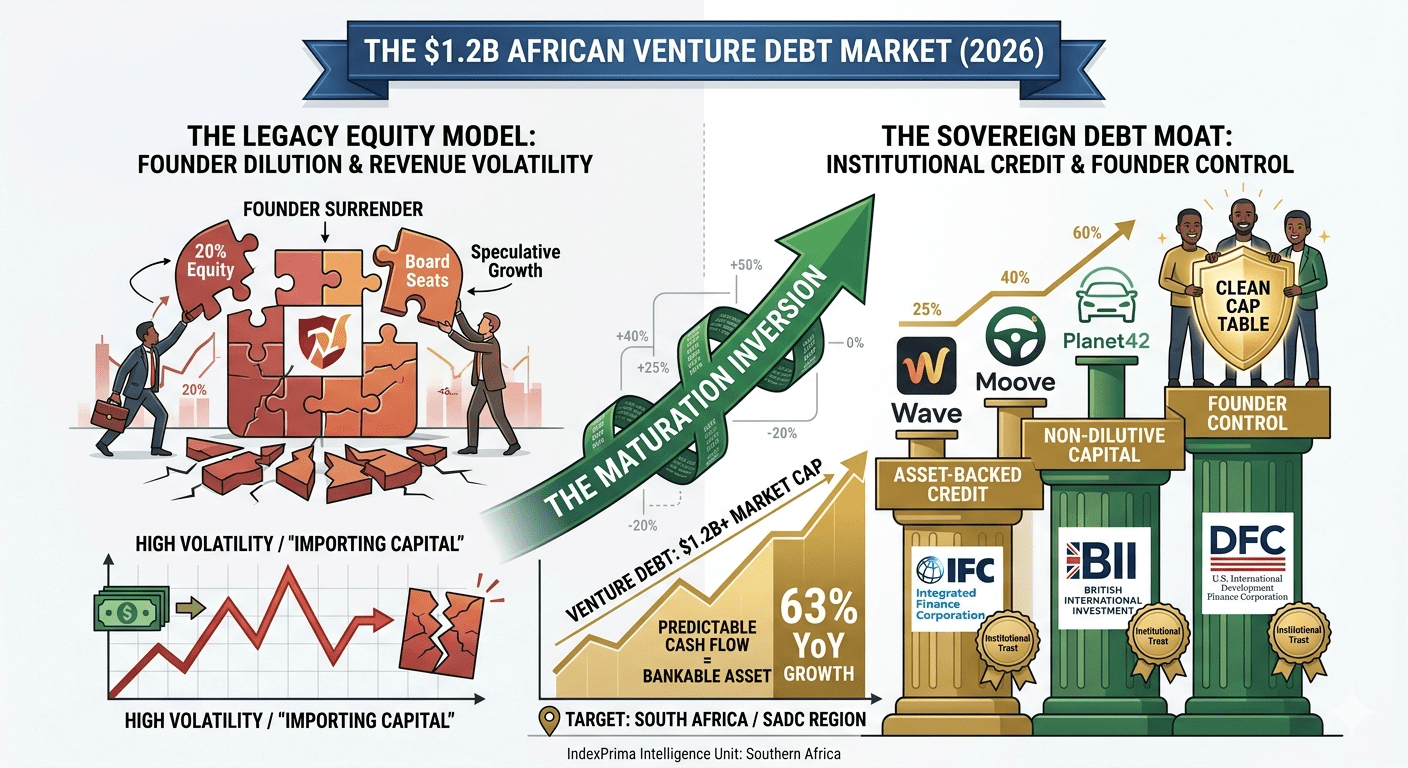

For years, the “African Tech Success Story” was measured by the size of the equity check. A Series B from a Silicon Valley VC was the ultimate signal of arrival. But in March 2026, the signal has shifted. The most sophisticated founders on the continent are no longer looking for “speculative fuel”—they are looking for “operational fuel.”

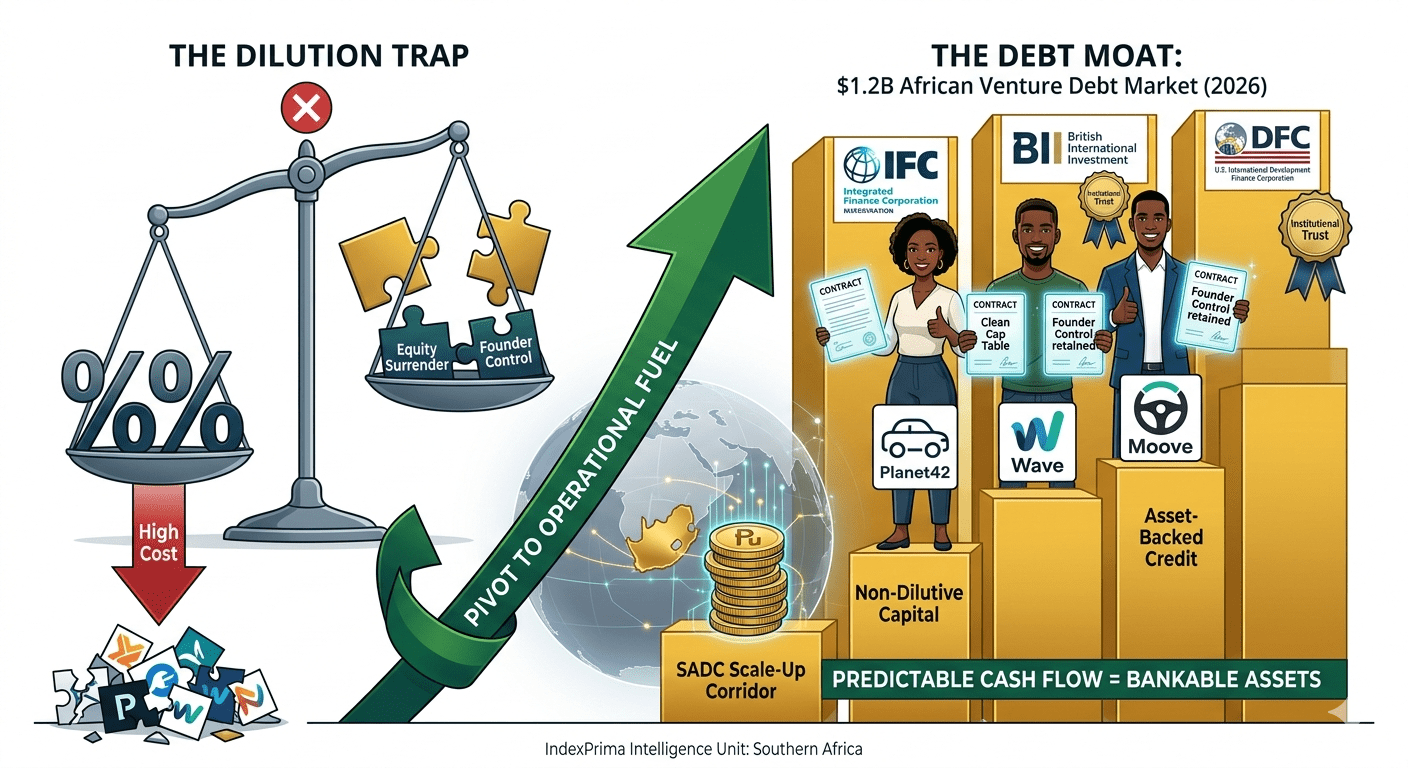

A structural transformation is sweeping through Southern Africa and the wider SADC region. As of Q1 2026, the venture debt market in Africa has matured into a $1.64 billion segment, growing by a staggering 63% year-on-year. Leading the charge are not just niche lenders, but the world’s most powerful Development Finance Institutions (DFIs)—the IFC, BII, and DFC—who have effectively institutionalized the market.

This is the Maturation Inversion: In an environment where equity is expensive and valuations are disciplined, debt has become the preferred “moat” for scale-ups to grow without surrendering the keys to the castle.

1. The Equity Squeeze: Why Dilution is the New Enemy

In the “growth at all costs” era of 2021, founders sold 20% of their company for a check that barely lasted 18 months. Today, the math has changed.

-

Ownership Retention: By raising debt instead of equity, founders of companies like Wave and Moove are keeping their cap tables clean. In 2025/2026, venture debt has reached 41% of all capital invested in African tech.

-

Cost of Capital: With interest rates for venture debt typically landing between 8% and 15%, it is significantly cheaper than the long-term cost of giving away a double-digit equity stake in a company potentially worth billions.

-

The “Bridge” Strategy: Founders are using structured credit to extend their “runway” between equity rounds, allowing them to hit higher valuation milestones before going back to the VC market.

2. The DFI Takeover: Institutionalizing the Risk

The entry of the International Finance Corporation (IFC), British International Investment (BII), and the U.S. International Development Finance Corporation (DFC) has brought a “Wall Street” level of rigor to Gaborone, Johannesburg, and Lagos.

Case Study: The Moove Mobility Moat

In late 2025, the mobility fintech Moove secured a massive debt facility backed by international lenders to expand its “Drive-to-Own” model across Southern Africa.

-

The Mechanism: Because Moove has predictable, daily cash flows from its fleet, it is a “bankable” asset.

-

The Result: The debt allows them to purchase thousands of new vehicles without raising a massive, dilutive Series C.

-

The Signal: This is the blueprint for the “Real Economy” startups—those with physical assets (cars, solar panels, inventory) are now winning the debt war.

Case Study: Planet42 and the Credit Algorithm

South Africa-based Planet42, which focuses on car subscriptions for the underserved, has systematically replaced early equity with large debt tranches from institutional private credit funds. By leveraging their proprietary AI credit-scoring model, they proved to lenders that their “default risk” was lower than traditional banks perceived, unlocking millions in non-dilutive capital to scale across the SADC region.

3. The Regional Divide: Southern Africa’s Equity Depth

While Kenya leads the continent in pure debt volume (driven by massive Cleantech deals), South Africa remains the “Equity Anchor.”

-

The South African Model: In 2025, South Africa reclaimed its spot as the #1 equity market, raising $643M in venture equity.

-

The Convergence: We are now seeing a “Hybrid Model” in Johannesburg. Startups raise an equity “Seed” to build the tech, then layer on a “Debt Growth” facility as soon as they hit $1M in Annual Recurring Revenue (ARR).

4. The Age of the “Scaler”

We have entered a two-tier ecosystem.

-

The Builders: Early-stage startups still rely on the “speculative fuel” of equity.

-

The Scalers: Mature companies with cash-flow visibility are moving to debt.

The Africa Funding Matrix 2026

| Feature | Traditional VC (Equity) | Venture Debt (Credit) |

| Stage | Seed / Series A | Series B / Growth / Scale-up |

| Requirement | Vision & Growth Narrative | Cash Flow & Asset Visibility |

| Cost | High (Ownership Dilution) | Moderate (8-15% Interest) |

| Control | Board Seats / Veto Rights | Covenants / Repayment Terms |

| Dominant Sector | Software / Pure-play AI | Fintech / Cleantech / Mobility |

Sources & Intelligence References

-

Market Analysis: 2025 Africa Tech Venture Capital Report (Partech, Jan 22, 2026).

-

Institutional Data: IFC Commits Record $71.7 Billion to Private Sector in FY2025 (IFC, 2026).

-

Venture Intelligence: Venture Debt Surpasses Equity for African Scale-ups (BusinessDay NG, March 25, 2026).

-

Case Study Archive: Planet42 and the Evolution of South African Private Credit (TechCabal Insights, 2025/2026).

Venture debt is no longer a “fringe” instrument; it is the core pillar of the African tech comeback. For the first time, African founders are proving they don’t just know how to “spend” capital—they know how to “manage” it. The era of the “Dilution Trap” is officially over for those with the revenue to prove it.

{kind=link}