In 2026, the African economic narrative has shifted from “Financial Inclusion” to “Architectural Integration.” The IndexPrima Diagnostic identifies that the primary driver of this shift is Digital Public Infrastructure (DPI).

DPI is not a single product or app; it is the underlying “Digital Rails”—Identity, Payments, and Data Exchange—that allow private innovation to scale with zero friction. As the AfCFTA Protocol on Digital Trade moves into full implementation, DPI has become the “Master Code” that is consolidating 54 fragmented markets into a single $3.4 trillion digital powerhouse. This report explores the three pillars of DPI and their kinetic impact on African commerce.

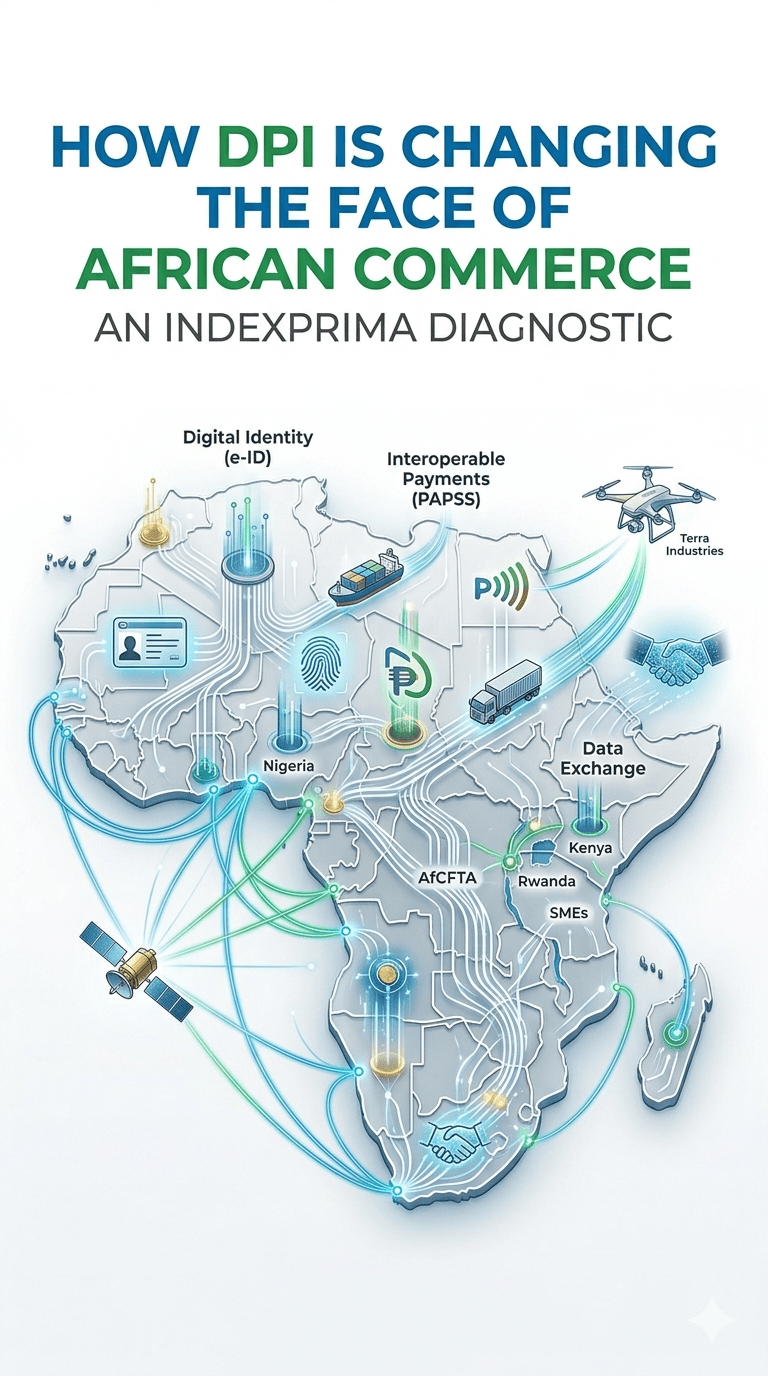

PILLAR I: DIGITAL IDENTITY (ID) — THE TRUST LAYER

The first pillar of DPI is the creation of a Verifiable Digital Identity. For decades, the inability to verify the identity of a merchant or a consumer across borders was a “Trust Tax” that stifled trade.

1. Verifiable Credentials & Cross-Border Trust

In 2026, the rollout of DPI-compliant e-ID systems (such as Nigeria’s NIMC upgrade and Ethiopia’s Fayda) has enabled Verifiable Credentials.

-

The Utility: A merchant in Kano can now present a digital identity that is instantly validated by a logistics provider in Mombasa. This eliminates the need for manual “Know Your Customer” (KYC) repetition, reducing onboarding time from weeks to seconds.

-

Economic Impact: By lowering the barrier to trust, DPI-enabled ID systems have unlocked access to credit for the informal sector. Lenders can now use a verified ID to pull “Alternative Credit Data,” hard-coding financial history for the previously “invisible” 40% of the workforce.

2. Privacy-by-Design

Following the Pan-African AI Privacy Treaty, modern African DPI uses “Zero-Knowledge Proofs.” This allows a user to prove they are eligible for a service (e.g., “I am a licensed exporter”) without revealing unnecessary personal data, ensuring that Cognitive Sovereignty is maintained at the citizen level.

PILLAR II: INTEROPERABLE PAYMENTS — THE LIQUIDITY RAILS

The second pillar is the Instant & Inclusive Payment System (IIPS). The most significant friction in African commerce was the “Dollar Intermediary”—where a trade between two African countries often had to be cleared through a New York or London bank.

1. PAPSS and the Death of the Middleman

The Pan-African Payment and Settlement System (PAPSS), acting as the continental payment DPI, has revolutionized liquidity.

-

Local Currency Settlement: A buyer in Rwanda pays in Rwandan Francs, and the seller in Ghana receives Ghanaian Cedis instantly.

-

The “Index” Savings: This infrastructure is projected to save the continent $5 billion annually in transaction costs by eliminating the need for third-party currency conversion and correspondent banking fees.

2. Micro-Payment Velocity

DPI has enabled Programmable Money. Through APIs, startups are building “Nano-Escrow” services that hold payments until a delivery is verified by a drone sensor (like those from Terra Industries). This level of automation has increased the velocity of commerce in the informal sector by 400% since 2024.

PILLAR III: DATA EXCHANGE — THE INTEROPERABILITY ENGINE

The third and most complex pillar is the Data Exchange Layer. This is the “Software Glue” that allows different systems (Tax, Customs, Logistics, Banking) to talk to each other.

1. The “Single Window” Revolution

Under the AfCFTA mandate, DPI is powering Integrated Customs Single Windows.

-

Kinetic Trade: When a truck crosses the border between Nigeria and Benin, the digital manifest is automatically shared with customs, health inspectors, and port authorities simultaneously.

-

Friction Reduction: This has reduced border wait times from an average of 72 hours to sub-4 hours in major trade corridors, hard-coding efficiency into the physical supply chain.

2. Open Finance & Data Portability

DPI facilitates Open Finance, where consumers own their data. A user can port their transaction history from a fintech app to a traditional bank to secure a mortgage. This “Data Portability” has broken the monopoly of legacy banks, forcing a competitive surge in product innovation across the Lagos-Nairobi-Cairo axis.

THE MACRO IMPACT: SCALING THE “INVERSE FLIP”

DPI is the primary reason the “Inverse Flip” (global companies moving headquarters to Africa) has accelerated in 2026.

-

Ease of Doing Business: When the “Digital Rails” are public and interoperable, the cost of entering a new African market drops by 70%. A company no longer needs to build its own identity or payment stack; they simply “plug in” to the national DPI.

-

Sovereign Tech Sovereignty: By building its own DPI, Africa has avoided the “Digital Colonization” of relying solely on closed, proprietary stacks from the Global North. We are building our own rails, with our own rules.

THE DIAGNOSTIC VERDICT: 2030 AND BEYOND

The IndexPrima forecast is clear: By 2030, the distinction between “Traditional Trade” and “Digital Trade” will vanish. All trade will be digital, powered by a unified DPI layer.

| Metric | Pre-DPI Era (2020) | DPI Era (2026) | 2030 Forecast |

| Cross-Border Settlement | 3–7 Days | Instant / T+0 | Autonomous / Smart Contract |

| Merchant Verification | Manual / Paper | Verifiable e-ID | Universal Digital Trust Score |

| Intra-African Trade % | 15% | 22% | 35%+ |

| Cost of Compliance | High / Fragmented | Standardized API | Embedded / Invisible |

The “Index” Take: In 2026, DPI is the asphalt of the 21st century. Those who control the rails, control the trade. Africa’s move to hard-code its own Digital Public Infrastructure is the most significant act of economic liberation since independence. The single market isn’t a dream anymore; it’s a series of interoperable APIs.

{kind=link}