The narrative surrounding African venture capital has officially graduated from the speculative hype of the pandemic-era boom and the subsequent panic of the “funding winter.” Data from the close of 2025 and the opening quarter of 2026 confirms that the market is no longer in freefall; it has recalibrated.

According to consolidated ecosystem indices from Partech Africa, AVCA, and Briter Bridges, African tech startups clawed their way back to a resilient $3.9B to $4.1B in total financing (equity and debt combined) by the end of last year. Moving into H1 2026, momentum has sustained, with January and February alone pulling in $575 million—a 26.5% increase over the same period last year.

However, the architecture of this capital deployment has fundamentally changed. The profile of the backers, the geographic distribution of the checks, and the underlying investment theses have flipped.

1. THE WHO: The Rise of the Local Balance Sheet & the Debt Syndicate

The most significant structural shift in African venture finance is the identity of the entities writing the checks. The era of the “Silicon Valley tourist”—foreign funds deploying capital via zoom calls based on Western metrics—has contracted. In their place stands a mature, highly disciplined network of domestic LPs and specialized debt providers.

-

Domestic LP Dominance: According to AVCA’s latest insights, domestic investor participation hit an all-time high. African investors (primarily regional corporates, local high-net-worth families, and African Development Finance Institutions) accounted for 45% of total venture fund commitments, a massive leap from the 23% average tracked between 2022 and 2024.

-

The Rise of the Debt Machine: Equity is no longer the sole king of the capital stack. Venture debt doubled to $1.8 billion, becoming a core stabilizing instrument rather than an afterthought. Growth-stage companies are aggressively utilizing debt to extend runways, manage equity dilution, and fund asset-heavy operations. In Q1 2026 alone, debt volume expanded sixfold year-on-year, while equity transactions remained highly disciplined.

-

Institutional Consolidators: Tier-1 pan-African managers like Partech Africa and Ingressive Capital remain central to early and growth stages, alongside strategic global corporates like Japan’s Sumitomo Corporation, which are leading massive, hundred-million-dollar late-stage interventions.

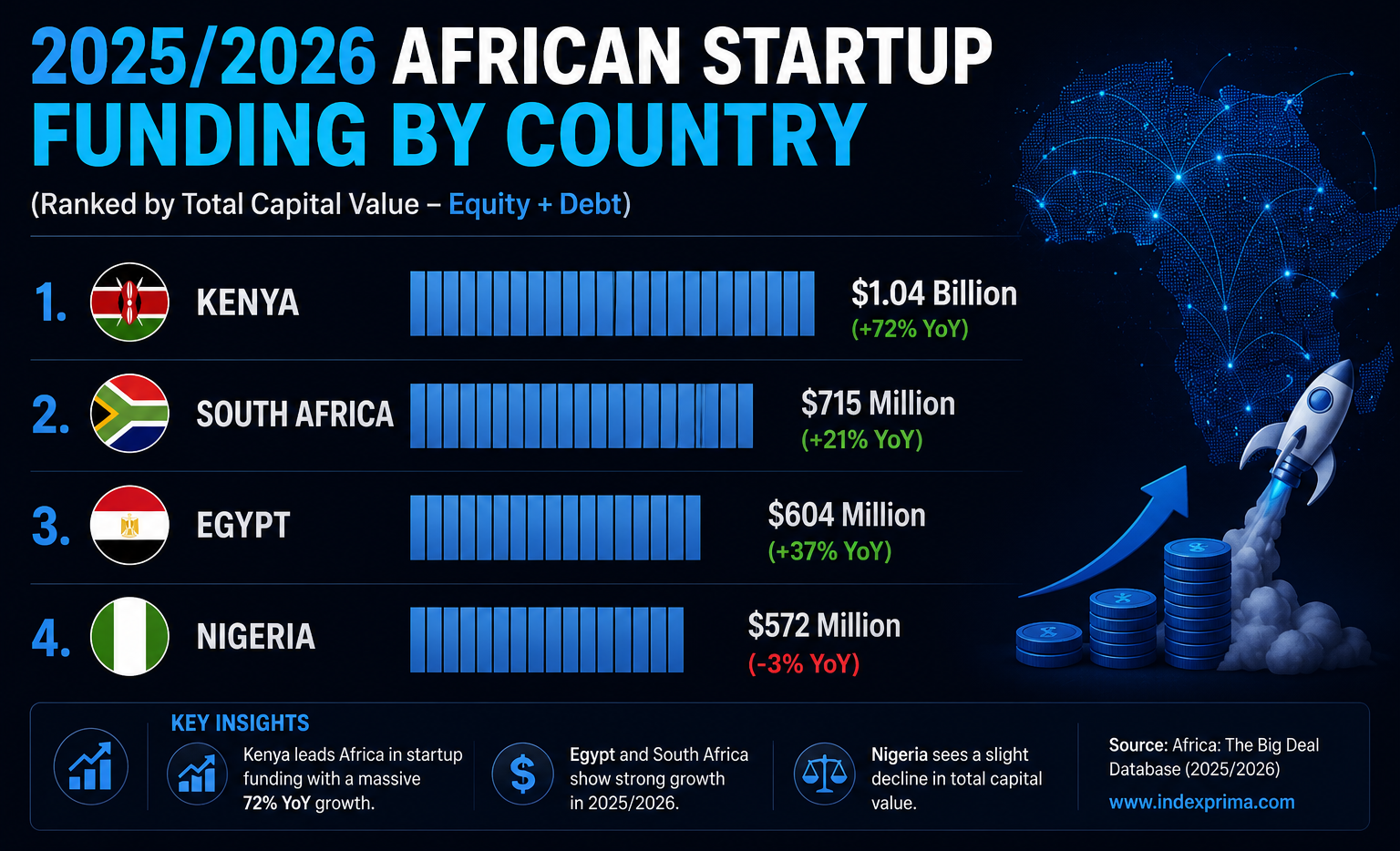

2. THE WHERE: The Changing Topography of the “Big Four”

While the historic “Big Four” tech hubs (Kenya, South Africa, Egypt, and Nigeria) still command over 72% to 82% of total continental funding, the internal hierarchy within this group has undergone a dramatic shakeup.

2025/2026 AFRICAN STARTUP FUNDING BY COUNTRY

(Ranked by Total Capital Value - Equity + Debt)

1. KENYA |||||||||||||||||||||||| $1.04 Billion (+72% YoY)

2. SOUTH AFRICA ||||||||||||||||| $715 Million (+21% YoY)

3. EGYPT |||||||||||||| $604 Million (+37% YoY)

4. NIGERIA ||||||||||||| $572 Million (-3% YoY)

Kenya’s Infrastructure Breakout

For the first time, Kenya has seized the absolute number-one spot on the continent, crossing the $1.04 billion mark. Kenya’s dominance is uniquely driven by its alignment with the global climate-tech agenda and a surge in asset-backed late-stage debt financing.

South Africa’s Deep Liquidity Moat

South Africa ranked as the number-one market for pure equity funding ($643 million across 85 rounds). Its mature corporate landscape, deep domestic banking integration, and structural stability have made it a safe haven for institutional investors looking for predictable revenue models in fintech and insurtech.

Egypt’s North African Resilience

Egypt maintained its steady upward trajectory, securing over $600 million. The ecosystem has effectively leveraged its position as a dual gateway to both the African continent and the Middle East, capturing capital from cross-border Gulf syndicates.

Nigeria’s Capital Decompression

Nigeria recorded a minor capital contraction, slipping to fourth in total funding value at $572 million. However, this decline is deceptive: Nigeria still recorded the highest absolute volume of individual deals across Africa. The market is shifting toward a high-volume, lower-ticket seed and pre-seed environment, moving away from hyper-inflated, late-stage equity valuations.

3. THE WHY: The Pivot to Hard Assets and Applied Utilities

Why are investors deploying capital right now? The macroeconomic thesis has shifted from speculative, software-only B2C consumer plays to physical infrastructure, asset-heavy cleantech, and B2B operational efficiency.

| Sector Vertical | 2025/2026 Trajectory | Strategic Investment Thesis |

| Cleantech & Climate | $1.18 Billion (+99% YoY) | Investors are backing asset-heavy, infrastructure-like models with highly predictable utility cash flows (e.g., pay-as-you-go solar networks like Sun King and electric mobility networks like Spiro). |

| Fintech | $1.49 Billion (-12% YoY) | While still the largest overall sector, fintech’s dominance has narrowed. Investors are fleeing basic digital wallets to fund deep credit infrastructure, merchant payment rails, and embedded B2B finance tools. |

| Applied Artificial Intelligence | Accelerating Value Share | Capital is entirely ignoring speculative, deep R&D LLM models. Instead, investors are aggressively funding startups that integrate AI as an operational efficiency layer to optimize risk management, clinical logistics, and agricultural supply chains. |

| Logistics & SME Enablement | Steady Consolidation | Startups building the physical distribution networks, cold-chain storage systems, and inventory automation software for the informal retail sector are receiving consistent growth-stage backing. |

The Index Take

The structural reconfiguration of capital flowing into Africa proves that the venture ecosystem has matured out of its infancy. The “funding winter” did not kill African tech; it systematically cleansed the market of undisciplined business models built purely on subsidized user acquisition.

The fact that venture debt has surged while local LPs now anchor nearly half of all fund commitments indicates that the continent is developing its own internal financial immune system. Investors are no longer buying vague promises of “unlocked consumer growth.” They are buying hard infrastructure, climate-resilient energy networks, and cash-generative B2B credit rails.

For founders navigating this new paradigm, the directive is unyielding: if your startup does not have a clear path to unit-economic profitability, or if your technology cannot be leveraged to solve a real-sector physical bottleneck, the capital markets of 2026 will pass you by. The money is there—but it is smarter, more local, and more demanding than it has ever been.