For decades, the “Franc Zone” has shared a currency but lacked a shared ledger. Despite the CFA franc’s stability, a merchant in Abidjan (UEMOA) trying to pay a supplier in Douala (CEMAC) has traditionally faced a gauntlet of “Foreign Exchange” fees and multi-day settlement delays.

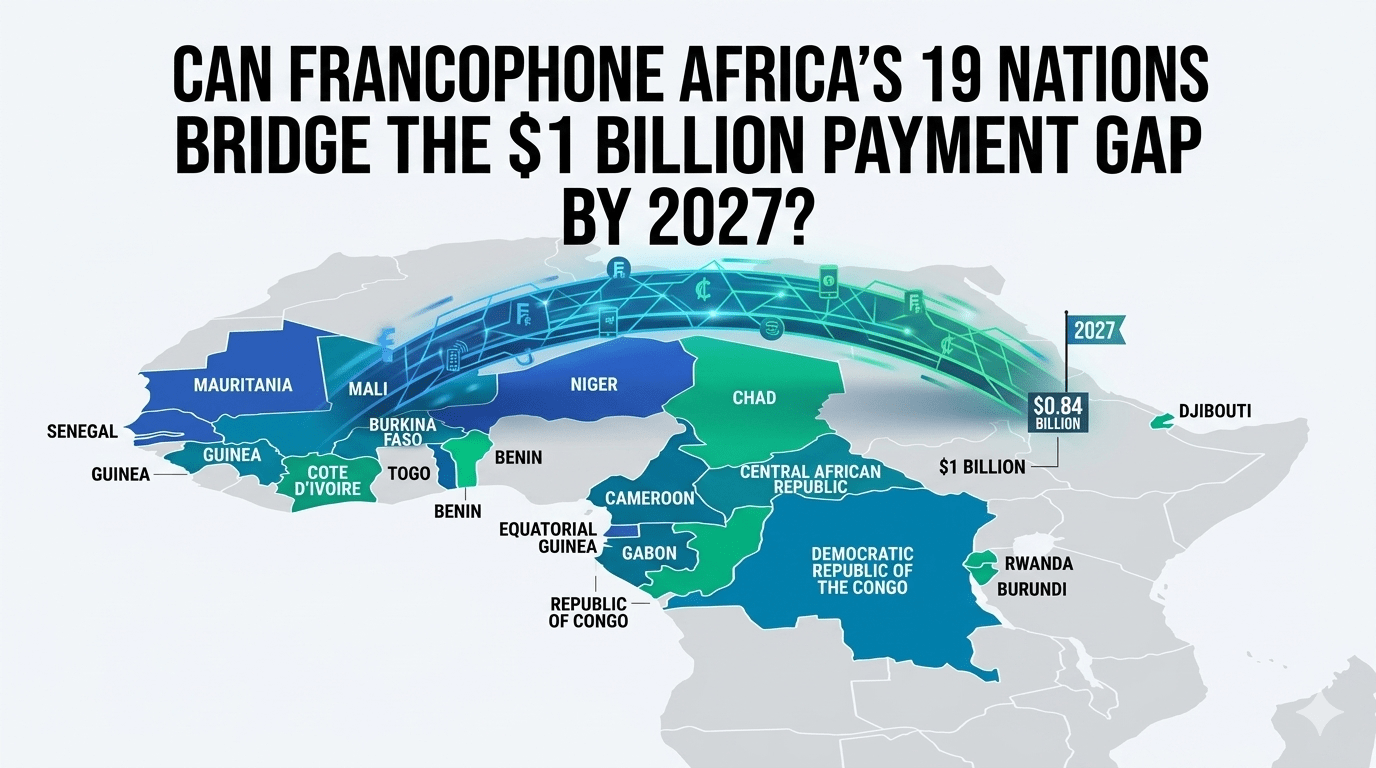

But as we approach 2027, the tide is turning. Driven by a new mandate for Francophone Interoperability, 19 countries are synchronizing their payment rails. This isn’t just a win for fintech—it is the unlock for $1 Billion in “Small-ticket” cross-border trade that has been trapped in the informal cash economy.

The technical backbone of this shift lies in the forced marriage of two regional giants: GIM-UEMOA (West Africa) and GIMAC (Central Africa).

-

The “GIMACPAY” Standard: Building on the success of Central Africa’s convergent ecosystem, the 2027 roadmap mandates a Convergent Instant Payment Rail that bridges cards, mobile money, and bank transfers across both zones.

-

The Single-API Layer: Companies like Hub2 and Cauridor are already deploying the “Market Integration Layer,” allowing merchants to accept payments from 19 different countries through a single technical integration.

Historically, small-scale cross-border trade in Africa has been “invisible” because it’s cash-based. The 2027 interoperability target aims to capture this “Small-ticket” volume—transactions between $50 and $500.

-

Informal to Digital: By lowering the cost of a cross-border transfer to near-zero, the 19 nations are migrating billions from the back of motorbikes into the digital banking system.

-

The SME Multiplier: For a small manufacturer in Senegal, the ability to receive instant payment from a buyer in Gabon without a 5% “remittance” fee is the difference between survival and scale.

The primary bottleneck isn’t code; it’s Policy.

-

The “Abuja Treaty” Momentum: Policymakers in BCEAO (West) and BEAC (Central) are finally aligning on “Privacy-by-Design” and KYC standards.

-

Regulatory Passports: The goal for 2027 is a “Regulatory Passport” that allows a licensed fintech in Togo to operate across the entire 19-country bloc without needing separate local licenses—a move that mimics the European SEPA model.

In the 2026 tech theater, “Remittance” is a dirty word. It implies a high-friction, one-way flow of capital. By 2027, Francophone Africa intends to replace “Remittance” with “Internal Transfer.” When a payment from Bamako to Brazzaville is treated with the same speed and cost as a local transfer, the 19-nation bloc ceases to be a collection of small markets and becomes a Continental Powerhouse.

Index Report: The 19-Nation Interoperability Vitals

| Component | Status | Strategic Significance |

| Market Scope | 19 Countries | UEMOA (8) + CEMAC (6) + peripheral partners. |

| Target Date | Q4 2027 | Full institutional and technical synchronization. |

| Trade Value | $1 Billion (est.) | Capturing informal small-ticket cross-border trade. |

| Tech Anchor | GIMAC / GIM-UEMOA | The unified interbank and mobile money switch. |

| Policy Goal | Regulatory Passport | One license for a 19-country digital market. |

The “Index” Take: Interoperability is the ultimate economic defense. By bridging the West and Central African zones by 2027, Francophone Africa is hard-coding its own internal trade resilience. In 2026, the winner isn’t the one with the best currency—it’s the one with the most integrated ledger.

Sources & References

-

Primary Outlook: GIMAC Regional Payment Innovation Report 2026

-

Policy Context: IMF eLibrary: Digital Payment Innovations in Sub-Saharan Africa

-

Market Infrastructure: Financial Afrik: Hub2 and Ecobank Cross-Border Partnership 2026